Euronext Dublin

Euronext Dublin

Irish indices

| Index | Last | % |

|---|---|---|

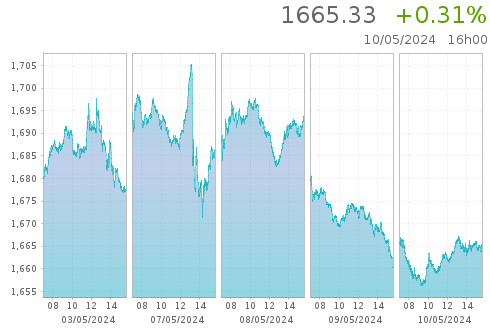

| ISEQ 20 | 1,619.97 | -1.32 % |

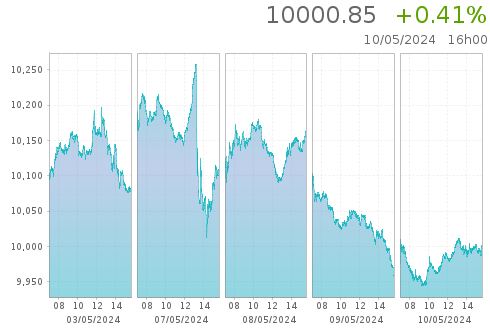

| ISEQ All Share | 9,778.52 | -1.21 % |

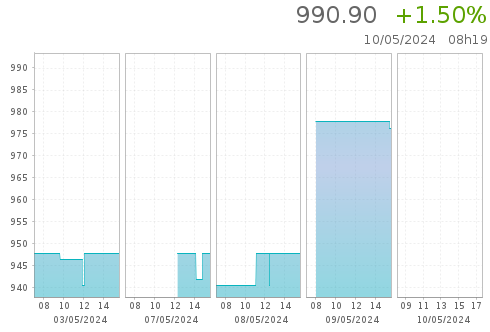

| ISEQ Small | 977.81 | -2.22 % |

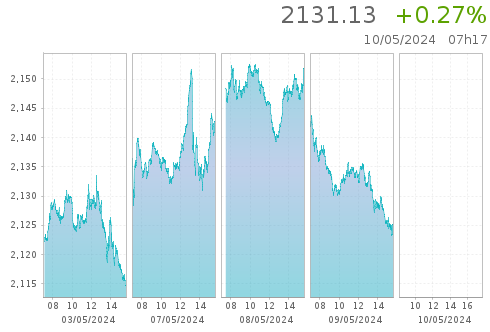

| ISEQ 20 Capped | 2,063.42 | -1.24 % |

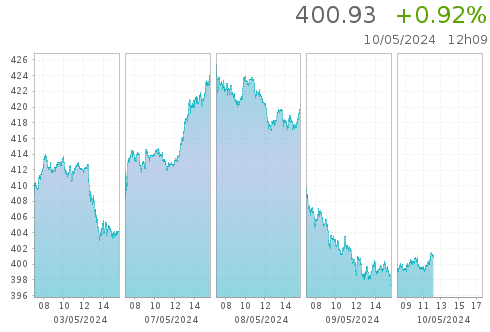

| ISEQ Financial | 390.67 | -1.38 % |

EU indices

| Instrument-name | Last-price | Day-change-relative |

|---|---|---|

| EURONEXT 100 | 1,501.87 | -1.29 % |

| CLIMATE EUROPE | 1,877.41 | -1.40 % |

| LOW CARBON 100 | 160.20 | -1.20 % |

| NEXT BIOTECH | 2,080.62 | -2.10 % |

| ESG 80 | 2,024.31 | -1.33 % |

Currency rates

| Instrument-name | Last-price | Day-change-relative |

|---|---|---|

| EUR / USD | 1.06205 | -0.06 % |

| EUR / GBP | 0.85438 | +0.08 % |

| EUR / JPY | 164.244 | +0.22 % |

| EUR / CHF | 0.9695 | +0.06 % |

| GBP / USD | 1.24307 | -0.11 % |

Irish indices

ISEQ 20

ISEQ ALL SHARE

ISEQ CAPPED

ISEQ FINANCIAL

ISEQ SMALL

Cash Products

More Euronext Dublin

Learn more about our Dublin markets

Visit our Dublin page on Euronext.com and learn about our Dublin offering.